Understanding Late-Stage Capitalism

A Systems Science Perspective

Peter Joseph is a filmmaker & author; host of the podcast Revolution Now! and one can support his open access work through Patreon or support here on Substack.

In the early twentieth century, the German economist and sociologist Werner Sombart coined the term “late capitalism” (Spätkapitalismus) across his multi-volume Der moderne Kapitalismus (1902–1927),1 using it to name the phase of capitalist society emerging from the wreckage of the First World War. Sombart never developed the idea into a systematic theory, and the term went dormant until economist Ernest Mandel revived it in Late Capitalism (1972; English translation 1975)2 to describe the postwar order of multinational corporations, financialization, and global integration. Fredric Jameson’s Postmodernism, or the Cultural Logic of Late Capitalism (1991)3 then carried the phrase into cultural theory...and the internet finished the job, turning “late-stage capitalism” into a shorthand for the absurdities of contemporary economic life.

Interpretations of what the idea means today range widely. For some, late-stage capitalism is less a precise economic diagnosis than a cultural mood. The Berkeley historian Trevor Jackson describes a pervasive post-1970s sense that something is profoundly broken — that we live surrounded by the wreckage of futures that never arrived.4 Annie Lowrey, writing in The Atlantic, traced how the phrase symbolized the indignities of modern economic life, where everyday experience feels increasingly shaped by corporate logic and commodification.5

Others approach the term more historically: The Conversation traces it to the “Marxist” political-economic tradition, where it denotes a mature phase of capitalism marked by monopoly power, global integration, financialization, and structural instability.6 And Jacobin, though sympathetic to capitalism’s critics, cautions against assuming that “late” means terminal, noting that capitalism has repeatedly shown an ability to mutate, absorb crises, and reconstitute itself in new forms.7

Taken together, these interpretations describe an atmosphere of exhaustion, instability, and contradiction. But from a systems-science perspective, the deeper question is not whether capitalism feels absurd or historically mature.

The deeper context, upon which this article will focus, is whether its inherently growth-dependent structure requires ever-greater inputs of debt, labor, energy, extraction, and ecological sacrifice simply to maintain its prior state—as a central, manifest force, pushing modern civilization into destabilization at an accelerating rate.

Hence our modern era of “late stage…" in more quantifiable, trend-rooted terms as they relate to civilizational collapse.

Understanding the System

First, let’s get to the bottom of a ubiquitous confusion: Capitalism is the attractor state of the endogenous dynamics of markets, not an imposed institution. Historians and academics have erroneously chopped up world history to delineate when “capitalism” first made itself known, generally focusing on when concentrations of private commercial power passed some subjective threshold. That approach may have merit at the institutional-observational level, but it is not a causal definition — and such definitions only hold weight if they embody causality.

In my own writing I have spent a great deal of time on the absurdity of the boxes and categories people have cobbled together to describe different historical economic conditions, past and present, since the Neolithic Revolution.

For the most binding causal attribute beneath all of them: is market-based trade.

It makes no difference how many thousands of years exchange goes back in time: the act of two parties trading property for differential advantage is the fertile substructure upon which our present condition has been built. (Even money itself, as the anthropologist David Graeber showed, is a relatively late arrival in that long story — the substructure precedes the medium.)8

It is unfortunate, and frankly regressive, that activists today continue to fall back on non-systemic framings, because doing so inhibits the ability to see the causal source of the vast majority of the world’s problems, from economic inequality to environmental destruction. I will not belabor that argument here; I have written about it extensively elsewhere.

The qualifier “late-stage” is different, however, because it implies that the system has undergone transformation. over time, by whatever measure. The measure I will put forward is best described as an entropy-like dynamic, tied to a core characteristic of market economics: the need for perpetual growth.

Now, in strict thermodynamic terms, entropy is a property of physical systems, and economies, like organisms, are open systems that can maintain their organization by drawing in energy and exporting disorder. The point is not that physics forbids an “organized economy.” The point, which is well documented, is that maintaining any organization has a cost, and that cost tends to rise with scale and complexity. Left to themselves, organized structures degrade. Resources disperse. Friction accumulates. Maintenance burdens increase. To preserve a system’s existing state requires continual inputs that offset these pressures.

This basic insight goes back to Nicholas Georgescu-Roegen’s The Entropy Law and the Economic Process (1971)9 — the founding work of ecological economics — formalized the economy as a throughput system that converts low-entropy resources into high-entropy waste, meaning every act of production carries an irreducible physical cost. And Joseph Tainter’s The Collapse of Complex Societies (1988)10 documented the complementary pattern across civilizations: societies tend to solve problems by adding complexity, and complexity yields diminishing marginal returns, until ever-larger investments are required merely to sustain prior levels of output and stability.

It is in this general sense that I apply the phrase “late-stage capitalism.”

Not as a moral judgment, but as a description of ever-increasing destabilization due to its endogenous processes - processes that define market economics, in particular… for market economics appears to have endogenous aspects that amplify the entropy process- namely its basis in economic growth.

And the critical question is not whether markets continue to function or profits continue to flow: it is what it now “costs” to keep them functioning, and whether that cost is rising faster than anything the system gives back (It is).

So viewed through this lens, late-stage capitalism is the stage at which growth increasingly ceases to represent progress and instead becomes compensation for mounting systemic costs the growth process itself created — what the ecological economist Herman Daly called uneconomic growth: growth whose costs exceed its benefits.11 The system must run faster merely to remain where it is… and on and on in a reinforcing loop.

And as we shall also see, this was precisely the dynamic that systems scientists at MIT began quantifying more than fifty years ago, when they examined the implications of exponential growth on a finite planet, as will be touched upon in a moment.

The Source of Growth

In stark contradiction to a litany of libertarian idealists that proudly promote the baseless assumption that the inherent structure of market economics does not necessarily lead to economic-material growth: market economies endogenously produce several overlapping growth imperatives that are not merely cultural preferences, political choices, or ideological commitments - they emerge from the internal operating logic of the market system itself and they can’t be stopped without destroying the society by which the market system is employed to ostensibly support.

I will state it again:

Market economies endogenously produce several overlapping growth imperatives that are not merely cultural preferences, political choices, or ideological commitments - they emerge from the internal operating logic of the market system itself and they can’t be stopped without destroying the society by which the market system is employed to ostensibly support.

Keep this summational proposition in mind.

Now. The three most foundational mechanism are the debt-and-interest system, competitive self-regulation, and more powerfully, cyclical consumption through the labor-income loop.

Each appears distinct at first, but in practice they merge into one unified growth requirement. Around them, secondary growth drivers arise (consumer culture, and government stimulus after crises) further reinforcing the system’s dependence on expansion.

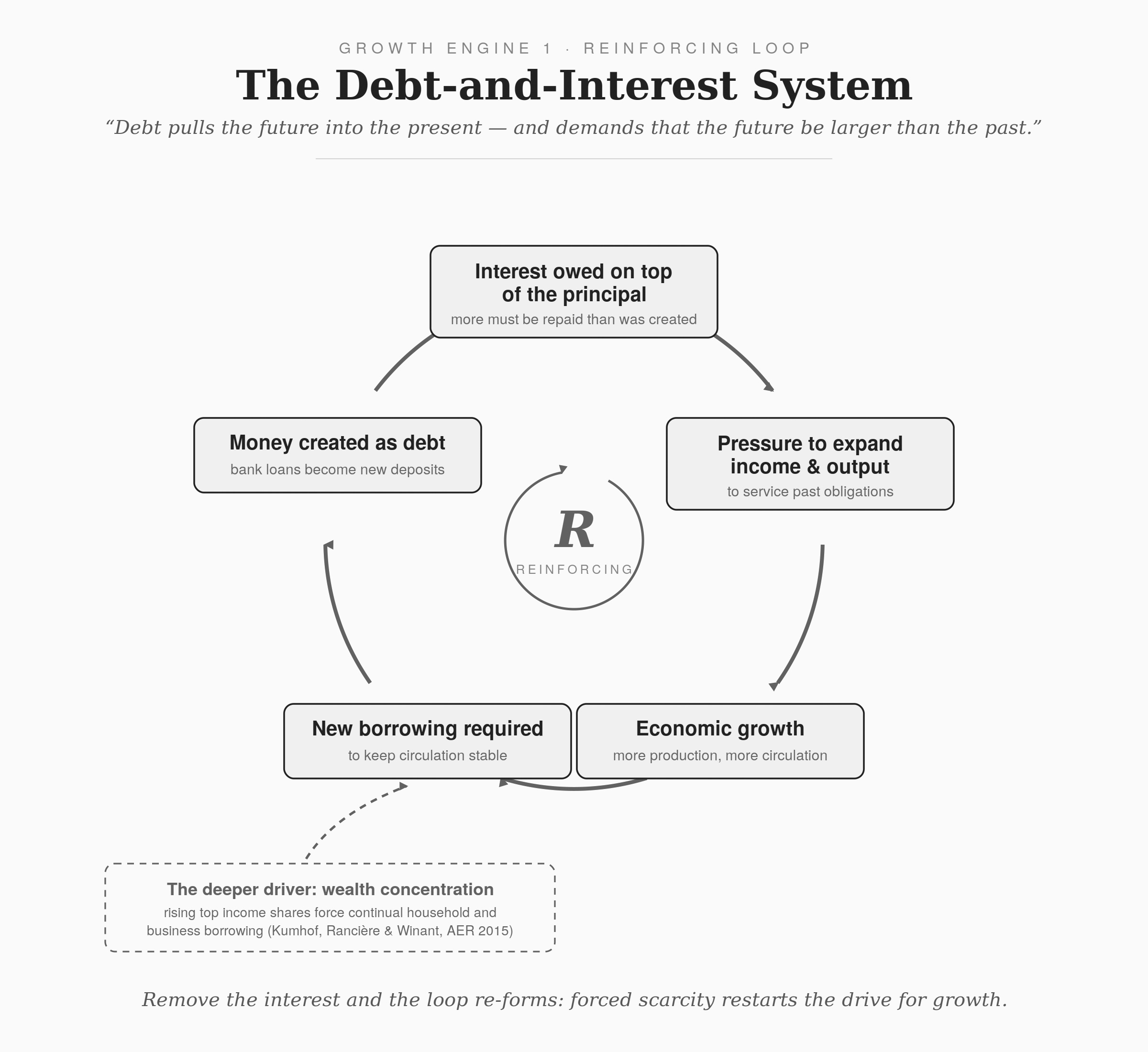

1. The Debt-and-Interest System

The first growth engine is the monetary structure itself. And it is worth stressing that this structure is a self-organizing subsystem of the market economy’s own evolution — not a deliberate policy decision by which global society sat down and chose to arrange things this way. Debt-money accreted over centuries from commercial practice; merchant credit, bills of exchange, goldsmith notes and states later codified and backstopped what practice had already built, through bank charters, legal tender laws, central banks, and deposit insurance. The policy layer ratified the system; it did not design it.

In modern economies, the overwhelming majority of money is created through debt. A fact confirmed by no less an authority than the Bank of England, whose 2014 paper “Money Creation in the Modern Economy” describes how commercial banks create new deposits in the very act of lending.12 Loans are issued, debt obligations are generated, and interest must be repaid on top of the original principal. This means economic actors are not simply required to repay what was created. They are required to generate an additional surplus beyond it.

At the level of an individual borrower, this may seem manageable. A person borrows money, earns income, and repays the loan with interest. But at the system level, the problem becomes more complex. The economy as a whole is placed under constant pressure to expand future production, future income, and future monetary circulation in order to meet past obligations.

While it is true that complex, circular velocity patterns in a large economy can pay back loans repeatedly with “the same money” and hence some level of alleviation occurs, this is not sufficient to cover the total liability that promotes more growth, as all empirical evidence proves when thinking about outstanding debt vs money supply vs debt servicing patterns, statistically. There is always a pressurized deficit.

It is not that every loan is impossible to repay. Rather, the system structurally depends upon continual new borrowing, continual new income generation, and continual economic expansion to prevent debt burdens from becoming destabilizing. Debt pulls the future into the present and then demands that the future be larger than the past.

The intuition is ancient. The disciplinary power of debt runs through five millennia of recorded history (David Graeber’s Debt: The First 5,000 Years traces it8) and premodern societies institutionalized periodic debt Jubilees precisely because they recognized that obligations compound beyond any realistic capacity to repay. The Nobel chemist turned monetary critic Frederick Soddy made the modern version of the argument in the 1920s: debt grows exponentially by mathematical convention, while the real wealth that must service it decays by physical law.13

And it has been formalized. Mathias Binswanger’s circular-flow model of a credit economy14 found that positive growth is necessary in the long run simply for firms to earn aggregate profits. Below a threshold rate of growth, the business sector as a whole makes losses. The system does not merely prefer expansion. It depends on it.

This is partly why market economies are structurally growth-dependent. If growth slows, debt service becomes harder. Defaults increase. Investment contracts. Employment falls. Public revenues decline. The entire system begins to seize.

The same logic operates internationally. Nations placed under debt obligations are often forced to expand exports, privatize resources, open markets, cut public spending, or intensify extraction simply to remain solvent. Debt therefore becomes not only a financial mechanism but a geopolitical pressure system. It locks individuals, businesses, and nations into the same basic bind: grow, extract, produce, and monetize more or fall behind.

Now, this subloop is a powerful one in the world economy, but it is also one of the few that could, in principle, be altered to a fair degree by policy even though it emerged organically and is now vastly entrenched. It is conceivable to break with the foundational premise of markets, which is private ownership, and nationalize national and global banking sectors, fostering a methodology that could, at least in part, produce credit without interest attached. This is not fantasy: India nationalized its major banks in 1969, France did so in 1982, the Bank of North Dakota has operated as a public bank since 1919, and the idea of removing money creation from private profit-seeking has formal pedigree in the 1930s “Chicago Plan” revisited favorably in a 2012 IMF working paper.15

The probability of this occurring globally, however, is exceptionally low. Money is treated as yet another product to be bought and sold through the loan process, with interest serving as the profit markup. The banking industry’s own core profitability metric - the net interest margin, the spread between what a bank pays for funds and what it charges for loans - makes the point plainly: in structural terms, a bank is consistent with the average mom-and-pop shop, except that what it sells is loans rather than goods. (Orthodox theory adds that interest also prices “time and default risk,” which is true yet changes nothing about the structural role of the markup.)

But here is the deeper issue, and it is why monetary reform alone would not defuse this engine. Binswanger’s result describes the system as it actually exists; the underlying pressure, however, does not originate only in the interest charge itself. The vast imbalances created by market dynamics concentrate income and wealth so extravagantly that the necessity for average people to continually take on personal and business loans would never subside.

This is not speculation: research by Kumhof, Rancière, and Winant in the American Economic Review found that in both 1920–1929 and 1983–2008, a rising income share at the top produced rising debt leverage among low- and middle-income households, ending in financial crisis — with the leverage emerging endogenously from the concentration itself.16 Even if all interest were removed from the system, this disproportionality would gravitate the system back to the same forced-scarcity pattern by which growth is initiated. There is simply no balance occurring; economic failure concentrates heavier debt burdens on those least able to carry them, and that scarcity forces the drive for growth once again.

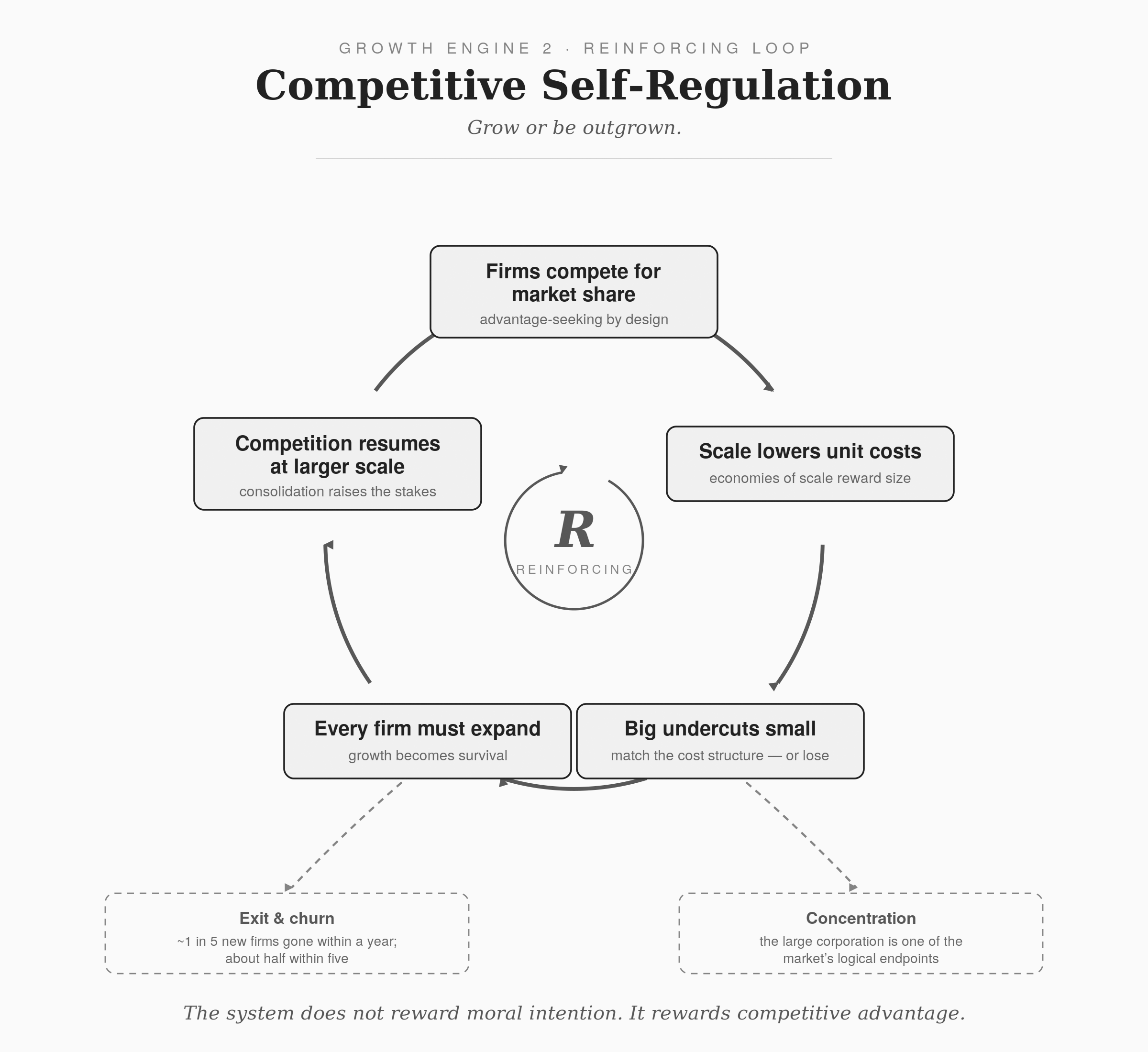

2. Competitive Self-Regulation: Grow or Be Outgrown

The second growth engine is competition. This one is absolutely ironclad: it cannot be regulated away in any form without changing, literally, the defining dynamic of market interaction itself, which is inherently competitive and advantage-seeking.

As we know, market theory often presents competition as a self-regulating force that keeps prices low, disciplines inefficiency, and benefits consumers. But from a systems perspective, competition generates a relentless expansionary pressure.

A firm operating in a competitive market cannot simply decide to remain small, stable, and content indefinitely if its rivals are expanding. Larger firms can often reduce unit costs through economies of scale, purchase inputs more cheaply, automate more aggressively, absorb losses longer, advertise more heavily, lobby more effectively, and capture distribution channels.

The small firm may be ethically superior, locally embedded, and socially useful. But if it cannot match the cost structure, reach, or efficiency of a larger competitor, it is vulnerable to being outperformed. The system does not reward moral intention. It rewards competitive advantage.

This is the “grow-or-die” principle and it is not rhetoric. The sociologist Erik Olin Wright identified economies of scale as the one unambiguous structural growth imperative at the firm level: remain small, and your unit costs remain permanently higher than those of your expanding rivals, until you are undercut.17 Myron Gordon and Jeffrey Rosenthal demonstrated the dynamic formally, showing through simulation that a firm pursuing a no-growth policy in a competitive environment faces near-certain bankruptcy over the long run.18

A business must expand market share, improve productivity, reduce costs, increase output, or otherwise strengthen its position. If it does not, another firm likely will. In this sense, there is no fundamental strategic difference between the small shop and the multinational corporation. They are playing the same game at different scales. The large corporation is not an aberration of the market. It is one of the market’s logical endpoints.

This is why corporate concentration is not simply the result of greed. Greed exists, of course, but the true issue is structural. Competitive markets reward scale, accumulation, and expansion. Over time, successful firms consolidate power, while unsuccessful firms disappear.

The enormous rate of business failure, roughly one in five new firms gone within a year, about half within five, is usually treated as a sign of healthy market selection. But from another perspective, it is a vast waste of human energy, material resources, planning effort, and social stability. The system produces endless duplication, rivalry, advertising manipulation, redundant infrastructure, and strategic sabotage, all in the name of efficiency.

Competition therefore becomes another growth imperative. Firms must grow to survive, and the economy must grow to absorb the consequences of that survival struggle.

3. Cyclical Consumption: The Labor-Income Loop

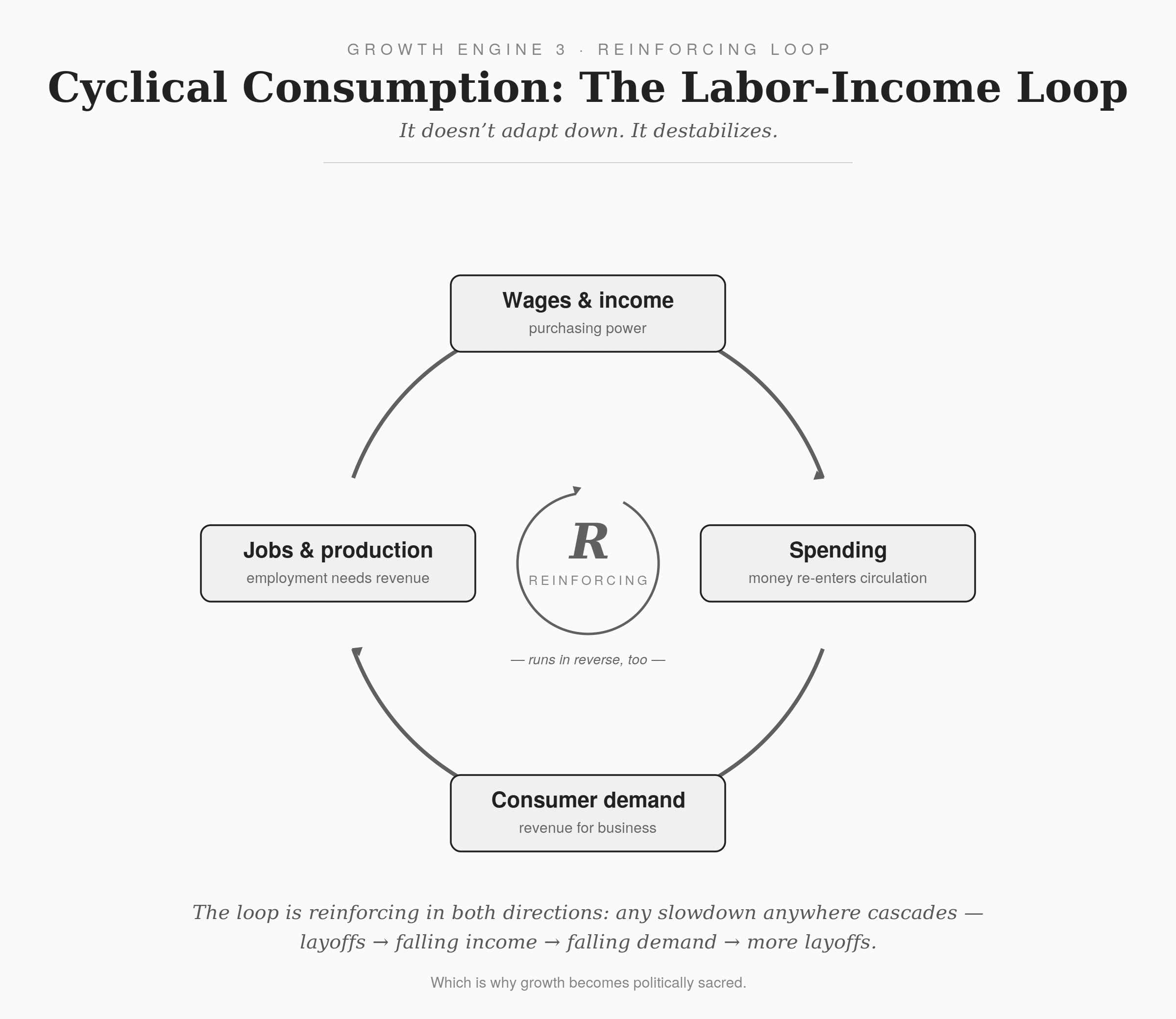

The third growth engine is the most foundational and easy to understand: cyclical consumption.

In a market society, people gain access to the means of life through income. Income generally comes through employment. Employment depends on business revenue. Business revenue depends on consumer demand. Consumer demand depends on purchasing power. Purchasing power depends on income.

This creates a circular dependency: wages generate spending; spending generates demand; demand generates jobs; jobs generate wages.

If any part of this loop slows, the entire system shuts down. If people stop buying, businesses lose revenue. If businesses lose revenue, workers are laid off. If workers are laid off, purchasing power declines. If purchasing power declines, demand falls further.

This is why contraction is so dangerous under current arrangements. The system is not designed to gracefully reduce unnecessary production. It is designed to maintain and accelerate monetary circulation. It doesn’t adapt down. It destabilizes.

Even socially useless activity can become economically necessary if it preserves employment and purchasing power. The classic absurdity is two people digging a ditch and filling it back in, each employing the other through meaningless labor. From a human or ecological perspective, nothing useful has been accomplished. But from a market perspective, wages were paid, income circulated, and economic activity occurred. This is not a strawman of market logic; it is market logic stated by its greatest defender. Keynes himself conceded that if the Treasury buried banknotes in bottles for private enterprise to dig back up, the resulting employment would be better than nothing, useful work being preferable, but circulation being the non-negotiable.19

This reveals a profound contradiction. A society that ties survival to employment must preserve activity for the sake of income, even when that activity is wasteful, destructive, or unnecessary.

This is the heart of the labor-for-income trap. The system cannot simply ask, “What do people need?” or “What is ecologically sustainable?” It must also ask, “How will people earn money?” As long as income is tied to market employment, and employment is tied to consumption, the economy is structurally biased toward endless turnover.

Tim Jackson named this bind precisely in Prosperity Without Growth (first a 2009 report for the UK Sustainable Development Commission, then a book now in its second edition).20 The consumerism that results from this growth requirement, he argued, functions as an “iron cage,” and the system faces a genuine dilemma of growth: growth is unsustainable, yet de-growth under present arrangements is unstable, threatening livelihoods the moment it begins. Environmental sociology reached the same conclusion from another direction in Allan Schnaiberg’s “treadmill of production” (1980):21 the faster the system runs, the faster it must run.

This is why growth becomes politically sacred. Without growth, jobs are threatened. Without jobs, income disappears. Without income, demand collapses. Without demand, businesses fail. And the cycle turns downward.

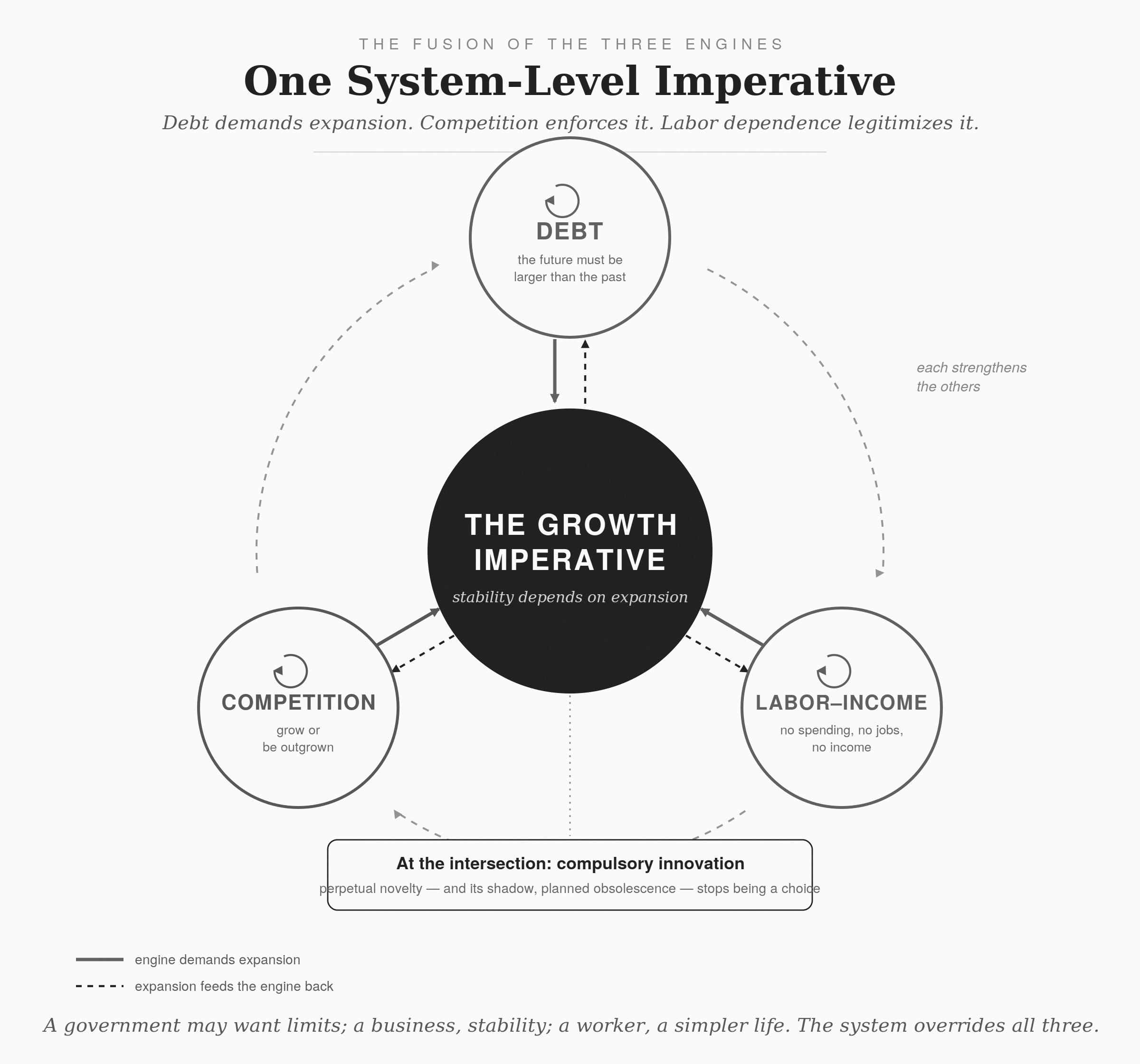

The Fusion of the Three Engines

Now: these three mechanisms do not operate separately. They fuse into one system-level imperative.

Debt requires future growth. Competition requires firm-level growth. Employment requires consumption growth.

Together, they form a self-reinforcing architecture. Debt demands expansion. Competition enforces expansion. Labor dependence socially legitimizes expansion. Each mechanism strengthens the others.

Even what we call innovation is largely a product of this fusion rather than a separate force: when survival requires selling and competition requires differentiation, perpetual novelty, and its shadow, planned obsolescence, stops being a choice and becomes compulsory.

A government may recognize environmental limits. A business owner may prefer stability over expansion. A worker may want a simpler life. A community may want less waste. But the system as a whole punishes these preferences when they conflict with monetary survival.

The market economy is organized so that stability itself depends on expansion.

4. Consumer Culture as a Secondary Growth Engine

Consumer culture emerges from this structure and then reinforces it.

Once an economy depends on continuous consumption, culture must be shaped to normalize continuous consumption. People must be trained to identify self-worth, success, freedom, status, and happiness with acquisition.

This is not an accidental development, and it is not human nature. The anthropological record is full of societies that actively suppressed acquisitive status display; insatiable materialism had to be cultivated. Industrial economies eventually became capable of producing far more than basic human needs required, and the problem then became how to absorb the surplus. Advertising, branding, planned obsolescence, status competition, and lifestyle marketing evolved, quite deliberately, as the early history of “consumption engineering” shows22 - as cultural mechanisms to keep demand moving.

Consumer culture therefore converts a structural economic requirement into a personal identity system. People do not simply buy objects. They buy symbols. They buy belonging, status, aspiration, security, novelty, and self-expression. The market colonizes psychology by turning identity into demand.

The obvious problem is that this demand has a material footprint. Every purchase carries behind it extraction, energy use, transportation, labor, waste, pollution, land use, water use, and disposal costs. According to United Nations resource data,23 the global material footprint — the raw material extracted to meet final demand — rose from 43 billion tonnes in 1990 to 92 billion tonnes in 2017, a 113 percent increase that outpaced both population growth and economic output. Per-capita extraction rose from 8.1 to 12.2 tonnes over the same period, with high-income nations consuming at more than double the global average. The cultural normalization of endless consumption is ecologically inseparable from the expansionary needs of the economy.

Consumerism is therefore not merely a moral failing or a shallow lifestyle preference. It is the cultural skin of the growth economy.

5. Stimulus After Crisis as a Secondary Growth Engine

The final reinforcing mechanism is crisis stimulus.

Market economies are prone to cycles of expansion and contraction. Financial bubbles, recessions, debt crises, unemployment shocks, and demand collapses recur with historical regularity. When contraction occurs, governments typically respond by trying to restart growth.

They inject liquidity. They lower interest rates. They bail out institutions. They subsidize demand. They stimulate consumption. They restore investor confidence. They attempt to re-employ displaced workers and reanimate the cycle of spending.

From a humanitarian standpoint, this is often understandable. People need income. Businesses are failing. Public panic is rising. Political leaders are under pressure to act.

But from a systems perspective, stimulus reveals the underlying dependency. When the growth machine stalls, the state intervenes to restart it. The goal is rarely to question whether the prior structure was rational, sustainable, or socially beneficial. The goal is to restore circulation.

This makes crisis management another growth-reinforcing mechanism. Each major downturn becomes an occasion to recommit society to the same expansionary model that produced the instability in the first place.

The system cannot tolerate prolonged contraction, because contraction threatens debt, employment, profits, tax revenues, asset values, and political legitimacy. So even when ecological realities demand reduced throughput, the economic structure demands renewed acceleration.

The Central Contradiction

The central contradiction is therefore simple: the biosphere requires balance, but the market system requires growth.

Period.

The planet operates according to physical limits, regenerative cycles, energy flows, and ecological thresholds. The economy operates according to debt obligations, competitive pressure, income dependency, consumer demand, and crisis recovery.

This is the deeper meaning of late-stage capitalism from a systems perspective. It is not merely inequality, corruption, corporate greed, or cultural absurdity. Those are symptoms. The deeper issue is that the system increasingly requires more debt, more extraction, more labor pressure, more consumption, more technological compensation, and more institutional intervention simply to maintain its existing state.

Growth, once framed as progress, becomes maintenance. Expansion, once framed as prosperity, becomes systemic self-defense.

And the more costly the system becomes to maintain, the more aggressively it must resist any ecological, social, or political constraint that threatens its expansion. This is why environmental regulation is weakened, debt is normalized, consumer culture is intensified, labor is disciplined, and crises are met with stimulus rather than structural redesign. The system is not behaving irrationally according to its own internal logic. It is behaving exactly as a growth-dependent system must behave when it begins to encounter limits.

The tragedy is that what is rational for the market is 100% irrational for life.

Enter “Late-Stage Capitalism”

In 1972, a team of systems scientists at MIT (Donella Meadows, Dennis Meadows, Jørgen Randers, and William Behrens) published The Limits to Growth,24 modeling the interaction of population, industrial output, food, resources, and pollution in a world of exponential growth and finite limits. What is commonly remembered is the headline: in the business-as-usual scenario, industrial growth stalls and reverses around the middle of the twenty-first century.

What is commonly missed is the mechanism. In the World3 model, decline does not arrive as a sudden external shock. It arrives as diminishing returns. As resource quality degrades and pollution accumulates, an ever-larger share of industrial output must be diverted to extraction, food production, and damage compensation. The surplus that once funded growth is progressively consumed by the cost of offsetting decline. Growth does not stop because anyone chooses to stop it. It stops because compensation eats it.

Fifty years on, the trajectory has held up. A 2021 recalibration by Gaya Herrington, published in the Journal of Industrial Ecology, found that observed world data tracks most closely with the model’s scenarios in which growth halts within roughly the next two decades.25

This is the entropy-like dynamic of the opening section, rendered in numbers — and it is what “late-stage” now properly names: a phase transition — the stage at which an expansionary system begins paying more to maintain itself than it gains by expanding. Rising debt loads that purchase less growth per dollar than they did a generation ago. Energy and extraction systems working harder for lower-quality returns. Technological compensation for problems that prior growth created. Institutions intervening ever more aggressively just to keep circulation alive.

It is tempting to stop there, on the reassuring note that nothing is scheduled and that systems in this condition could persist for a long time, absorbing shocks and reconstituting themselves, exactly as capitalism’s defenders point out.

But intellectual honesty requires following the logic to its end, and the end is inevitable without a kind of change that shuts down the exact growth parameters talked about in this article.

Lay the argument out plainly. The internal logic of the system, established across the preceding sections, is that it must grow — debt requires it, competition enforces it, the labor-income loop depends on it. The planet, however, cannot grow; it is a finite biophysical base. A system that cannot stop expanding, running against a base that cannot expand, has only two possible destinations: it transforms into something else, or it overshoots its limits and declines. There is no third option in which business as usual simply continues forever.

Now, as an aside, there is one commonly offered escape from this second destination that does not require deeper economic transformation: absolute decoupling — the idea that economic growth can be severed from material and energy throughput, allowing the economy to keep expanding while its physical footprint shrinks.

It is effectively the central hope of mainstream environmental policy. If absolute decoupling can occur globally, rapidly, and permanently, then the growth economy can, in principle, continue while ecological pressures decline.

But evidence tell a different story. Kallis’s “Is Green Growth Possible?” (2020),26 the European Environmental Bureau’s Decoupling Debunked (2019),27 and Haberl and colleagues’ systematic review of the decoupling literature (2020)28 all converge on the same basic conclusion: relative decoupling is real and common, meaning economies often become more efficient per unit of GDP. But absolute, sustained, economy-wide decoupling at the scale and speed required by ecological limits has not been observed.

In other words, the economy may adapt to using fewer resources per dollar of output here and there - but this does not mean total resource use, energy demand, pollution, and material throughput fall fast enough while growth continues. The burden of proof, therefore, remains with the green-growth thesis: it must show not merely that efficiency can improve, but that a continuously growing global economy can reduce its total ecological impact quickly enough to avoid systemic breakdown.

And this kind of thinking has its value in principle, but what is missed in all of the conversations supporting absolute and relative decoupling is the true nature of the market system environment we are actually in! The distinction between “growth” and “development” is an important one put forward by people like Donella Meadows, and Buckminster Fuller, and many others. But if you're trying to decouple within a system that will shut itself down if the decoupling take hold: there is no merit.

So! Today, we are no longer arguing from a 1972 simulation. The overshoot the model MIT projected is now directly measurable in the state of the planet’s life-support systems and yes: they are, without meaningful exception, in decline.

The planetary boundaries framework, the leading scientific assessment of the Earth-system processes that keep the planet habitable, finds that seven of nine boundaries have now been transgressed: climate change, biosphere integrity, novel entities, land-system change, freshwater use, biogeochemical flows, and, most recently, in 2025, ocean acidification, leaving only stratospheric ozone (slowly recovering) and aerosol loading inside the safe zone.29

Atmospheric CO₂ stands at roughly 425 parts per million against a proposed boundary of 350; ocean acidity has risen 30 to 40 percent since 1850, a rate roughly ten times faster than at any point in the last 55 million years.29 The living world is contracting in step: WWF’s 2024 Living Planet Index,30 drawing on nearly 35,000 monitored populations, records an average 73 percent decline in the size of monitored vertebrate populations between 1970 and 2020, with freshwater populations down 85 percent, terrestrial 69 percent, and marine 56 percent. (That figure is an average of proportional change across populations, not a count of individuals or species lost, but as an index of biosphere health, its direction is unambiguous.)

And the climate signal has crossed a threshold of its own: the World Meteorological Organization confirmed 2024 as the warmest year on record, at about 1.55 °C above pre-industrial levels and likely the first calendar year to exceed 1.5 °C, with the ten warmest years on record being the most recent ten.31

These are the World3 variables crossing into the red. No longer as a forecast, but as a measurement: a civilization drawing down the natural capital it runs on faster than that capital can regenerate.

Finally, a word on what “collapse” means.

It does not mean human extinction, and it does not mean an overnight apocalypse. In the World3 model, collapse is overshoot followed by involuntary, disorderly decline; falling industrial output and food per capita, falling population, the unwinding of complex systems a society can no longer afford to maintain. Joseph Tainter’s term for the same phenomenon is the rapid simplification of a society that can no longer pay for its own complexity.10 That is the meaning here, and it is grave enough without embellishment.

Following the chain to its end, the market system’s internal logic says it must grow. The biophysical record says the planet can no longer absorb that growth, and is visibly buckling under what it has already absorbed. The one, failed semi-mainstream mechanism often argued that could reconcile the two - decoupling - is, as shown, not materializing at the necessary scale nor can it.

Set those three facts beside one another, and the business-as-usual trajectory resolves to a single terminus: overshoot and decline, a forced and disorderly contraction of the human enterprise, amplifying, on current tracking, around the middle of this century.

I have looked hard for the argument that breaks this chain, and I have not found one that does not depend on a transformation that has not yet occurred - which can only go by the name system change. And I mean total system change.

If the drivers of growth are structural rather than political or social, they cannot be regulated away, taxed into submission, or moralized out of existence.

They can only be designed out and replaced by a system whose stability does not depend on its own expansion. That is why my closing question is no longer academic, and no longer optional: what would such an economy actually look like? On the trajectory we are on, that is not a thought experiment for some distant seminar. It is the whole of the difference between a transition we choose and undertake deliberately, and a contraction that arrives on its own terms and imposes itself upon us.

integralcollective.io

Peter Joseph is a filmmaker & author; host of the podcast Revolution Now! and one can support his open access work through Patreon or support here on Substack.

[1] Werner Sombart, Der moderne Kapitalismus, 3 vols. (Leipzig and Munich: Duncker & Humblot, 1902–1927).

[2] Ernest Mandel, Der Spätkapitalismus (Frankfurt: Suhrkamp, 1972); published in English as Late Capitalism, trans. Joris De Bres (London: New Left Books, 1975).

[3] Fredric Jameson, Postmodernism, or, the Cultural Logic of Late Capitalism (Durham, NC: Duke University Press, 1991).

[4] Trevor Jackson, interviewed in “What Does ‘Late-Stage Capitalism’ Really Mean?,” UC Berkeley News, March 31, 2026, https://news.berkeley.edu/2026/03/31/what-does-late-stage-capitalism-really-mean-uc-berkeley-professor-chronicles-an-apocalyptic-history/.

[5] Annie Lowrey, “Why the Phrase ‘Late Capitalism’ Is Suddenly Everywhere,” The Atlantic, May 1, 2017, https://www.theatlantic.com/business/archive/2017/05/late-capitalism/524943/.

[6] “We Live in a Time of ‘Late Capitalism.’ But What Does That Mean? And What’s So Late About It?,” The Conversation, December 2022, https://theconversation.com/we-live-in-a-time-of-late-capitalism-but-what-does-that-mean-and-whats-so-late-about-it-191422.

[7] See, for example, Vivek Chibber and Melissa Naschek, “Capitalism Won’t Collapse on Its Own,” Jacobin, May 2026, https://jacobin.com/2026/05/capitalism-crisis-collapse-socialism-determinism; and “Ernest Mandel and the Economics of Late Capitalism,” Jacobin, April 2023, https://jacobin.com/2023/04/ernest-mandel-marxist-economics-late-capitalism.

[8] David Graeber, Debt: The First 5,000 Years (Brooklyn, NY: Melville House, 2011).

[9] Nicholas Georgescu-Roegen, The Entropy Law and the Economic Process (Cambridge, MA: Harvard University Press, 1971).

[10] Joseph A. Tainter, The Collapse of Complex Societies (Cambridge: Cambridge University Press, 1988).

[11] Herman E. Daly, Beyond Growth: The Economics of Sustainable Development (Boston: Beacon Press, 1996).

[12] Michael McLeay, Amar Radia, and Ryland Thomas, “Money Creation in the Modern Economy,” Bank of England Quarterly Bulletin, Q1 2014, https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creation-in-the-modern-economy.

[13] Frederick Soddy, Wealth, Virtual Wealth and Debt: The Solution of the Economic Paradox (London: George Allen & Unwin, 1926).

[14] Mathias Binswanger, “Is There a Growth Imperative in Capitalist Economies? A Circular Flow Perspective,” Journal of Post Keynesian Economics 31, no. 4 (2009): 707–727, https://www.semanticscholar.org/paper/Is-there-a-growth-imperative-in-capitalist-a-flow-Binswanger/e0a4fe44d934a3028bf990c1f7eccb4f369a5186.

[15] Jaromir Benes and Michael Kumhof, “The Chicago Plan Revisited,” IMF Working Paper WP/12/202 (Washington, DC: International Monetary Fund, 2012), https://www.imf.org/external/pubs/ft/wp/2012/wp12202.pdf.

[16] Michael Kumhof, Romain Rancière, and Pablo Winant, “Inequality, Leverage, and Crises,” American Economic Review 105, no. 3 (2015): 1217–1245, https://www.aeaweb.org/articles?id=10.1257/aer.20110683.

[17] Erik Olin Wright, “Critique of Capitalism,” Sociology 621, Lecture 3 (University of Wisconsin–Madison, 2011), https://ssc.wisc.edu/soc/faculty/pages/wright/621-2011/lecture%203%20%202011%20-%20Critique%20of%20Capitalism.pdf.

[18] Myron J. Gordon and Jeffrey S. Rosenthal, “Capitalism’s Growth Imperative,” Cambridge Journal of Economics 27, no. 1 (2003): 25–48, https://academic.oup.com/cje/article-abstract/27/1/25/1713277.

[19] John Maynard Keynes, The General Theory of Employment, Interest and Money (London: Macmillan, 1936), ch. 10.

[20] Tim Jackson, Prosperity Without Growth? The Transition to a Sustainable Economy (London: UK Sustainable Development Commission, 2009); expanded as Prosperity Without Growth: Foundations for the Economy of Tomorrow, 2nd ed. (London: Routledge, 2017). The “iron cage” image adapts Max Weber’s famous phrase.

[21] Allan Schnaiberg, The Environment: From Surplus to Scarcity (New York: Oxford University Press, 1980).

[22] Roy Sheldon and Egmont Arens, Consumer Engineering: A New Technique for Prosperity (New York: Harper & Brothers, 1932); see also Stuart Ewen, Captains of Consciousness: Advertising and the Social Roots of the Consumer Culture (New York: McGraw-Hill, 1976).

[23] United Nations, The Sustainable Development Goals Report 2019 (New York: United Nations, 2019), Goal 12; see also UN Environment Programme / International Resource Panel, Global Resources Outlook 2019.

[24] Donella H. Meadows, Dennis L. Meadows, Jørgen Randers, and William W. Behrens III, The Limits to Growth (New York: Universe Books, 1972).

[25] Gaya Herrington, “Update to Limits to Growth: Comparing the World3 Model with Empirical Data,” Journal of Industrial Ecology 25, no. 3 (2021): 614–626.

[26] Jason Hickel and Giorgos Kallis, “Is Green Growth Possible?,” New Political Economy 25, no. 4 (2020): 469–486.

[27] Timothée Parrique et al., Decoupling Debunked: Evidence and Arguments Against Green Growth as a Sole Strategy for Sustainability (Brussels: European Environmental Bureau, 2019), https://eeb.org/library/decoupling-debunked/.

[28] Helmut Haberl et al., “A Systematic Review of the Evidence on Decoupling of GDP, Resource Use and GHG Emissions, Part II: Synthesizing the Insights,” Environmental Research Letters 15, no. 6 (2020): 065003.

[29] Katherine Richardson et al., “Earth Beyond Six of Nine Planetary Boundaries,” Science Advances 9, no. 37 (2023): eadh2458; ocean acidification was assessed as the seventh transgressed boundary in Planetary Boundaries Science Lab, Planetary Health Check 2025 (Potsdam: Potsdam Institute for Climate Impact Research, 2025),

https://www.planetaryhealthcheck.org/

[30] WWF, Living Planet Report 2024: A System in Peril (Gland, Switzerland: WWF International, 2024), https://www.worldwildlife.org/publications/2024-living-planet-report/.

[31] World Meteorological Organization, “WMO Confirms 2024 as Warmest Year on Record at About 1.55°C Above Pre-Industrial Level,” January 10, 2025, https://wmo.int/news/media-centre/wmo-confirms-2024-warmest-year-record-about-155degc-above-pre-industrial-level.

Peter Joseph, I don't know how you do it, put it seems that you wrote another blogpost that made me cry again, because the implications you mention in your post are insightful, frightening and hopeful at the same time.

Absolutely right on. Structurally self-perpetuating, no one driving the bus, with the Hotel Owners (at Life as a Game of MONOPOLY (TM) naturally motivated to play, and consumers likewise with few other sources of meaning given the torn fabric of belonging. See the movie Ancient Futures, for context.